CUET Preparation Today

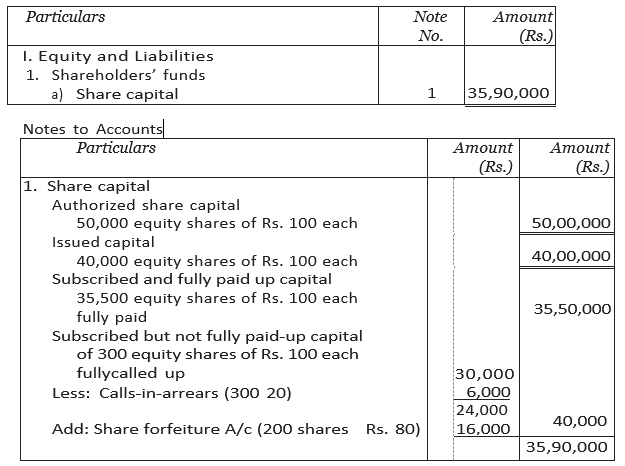

Select the correct sequence from the following : A. Issued capital B. Subscribed but not fully paid up capital C. Authorised capital D. Subscribed and fully paid up capital E. Share forfeited Account Choose the correct answer from the options given below : |

A, B, C, D, E B, A, C, D, E C, D, E, A, B C, A, D, B, E |

C, A, D, B, E |

The correct answer is option (4) : C, A, D, B, E. The following categories of capital in correct sequence is as follows- * C) Authorised Capital: Authorised capital is the amount of share capital which a company is authorised to issue by its Memorandum of Association. The company cannot raise more than the amount of capital as specified in the Memorandum of Association. It is also called Nominal or Registered capital. The authorised capital can be increased or decreased as per the procedure laid down in the Companies Act. It should be noted that the company need not issue the entire authorised capital for public subscription at a time. Depending upon its requirement, it may issue share capital but in any case, it should not be more than the amount of authorised capital. * A) Issued Capital: It is that part of the authorised capital which is actually issued to the public for subscription including the shares allotted to vendors and the signatories to the company’s memorandum. The authorised capital which is not offered for public subscription is known as ‘unissued capital’. Unissued capital may be offered for public subscription at a later date. * D & B) Subscribed Capital: It is that part of the issued capital which has been actually subscribed by the public. When the shares offered for public subscription are subscribed fully by the public the issued capital and subscribed capital would be the same. It may be noted that ultimately, the subscribed capital may be equal to or less than issued capital. In case the number of shares subscribed is less than what is offered, the company allots only the number of shares for which subscription has been received. In case it is higher than what is offered, the allotment will be equal to the offer. In other words, the fact of over subscription is not reflected in the books. Firstly the subscribed and full up capital is shown and after that if there is some partly paidup or partly called up amount then it is shown under the subscribed and not fully paidup capital. * E) Share forfeited Account- This account is prepared at last to cancel the already issued shares for the non payment of allotment or call money by shareholders. Their shares are cancelled by the directors. These shares can be reissued by the company. If after reissued any balance is left in the share forfeited account, it is transferred to capital reserve account.

|