CUET Preparation Today

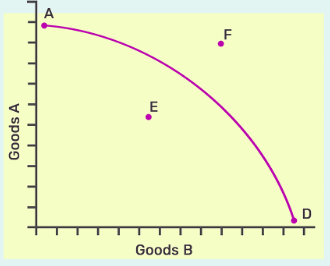

Consider an economy with fixed amount of resources and given technological state. It produces only 2 goods – Good A and Good B. Different combinations showing maximum outputs of two goods which can be produced (when given resources and technology are used fully) are plotted on a graph. When all the plotted points are joined, following graph was obtained.

Based on the above graph, answer the following questions. |

What does PPC show? |

ii, iv i, ii i, iii i, iii, iv |

i, iii, iv |

The correct answer is Option 4: i, iii, iv Here's why each option applies to PPC: i. Resources are limited: A core concept of PPC is that economies have limited resources (land, labor, capital) to produce goods and services. This limitation forces trade-offs. It is only because the resources are scarce that when we increase the quantity of one good produced, we have to decrease the quantity of another. That is why Production Possibility Curve is downward sloping. So Production Possibility Curve shows scarcity of resources. ii. Resources are unlimited (incorrect): PPC contradicts the idea of unlimited resources. The entire concept revolves around making choices due to resource constraints. iii. Opportunity cost: PPC clearly shows the concept of opportunity cost. As you choose to produce more of one good, you necessarily give up the opportunity to produce some amount of another good, due to limited resources. iv. Choice: PPC depicts the different choices an economy can make regarding production levels of two goods, given their resource limitations. Therefore, PPC showcases limited resources (i), opportunity cost (iii), and the choices available for production (iv). |